People hate inflation

And they don’t always think of ‘inflation’ in the same way that economists do.

Neither politics nor the US are really my beat, so from a purely selfish point of view I was hoping for a Harris win so that I wouldn’t have to address the election result here. But it wasn’t to be, and it feels like following it up with some post about quirky local data would just seem willfully out of touch.

You’ve probably already seen a lot of hot takes about why Trump was bound to win and/or why Harris was bound to lose. Bear in mind that pretty much all of these are things that were already known or believed before the election; the fact that they were true, and yet the polling was consistently quite close, should tell you that they aren’t the slam-dunk arguments that people would have you believe.

That said, it’s still worth digging through what some of those reasons were. There is inevitably some self-interest behind this - culture warriors will tell you it was about the culture wars, economists will tend to emphasise the economy, and so on. The obvious way to resolve this would be to ask voters directly, though that still relies on them being honest about who they voted for, as well as their reasons for it.

A post-election survey by Blueprint asked people to rank the importance of their reasons for not voting for Harris. Top of the list: “Inflation was too high under the Biden-Harris administration”. So score one for the importance of economics, though it wasn’t the one defining issue - it was basically tied with illegal immigration, and yes, ‘wokeness’ was right up there too.

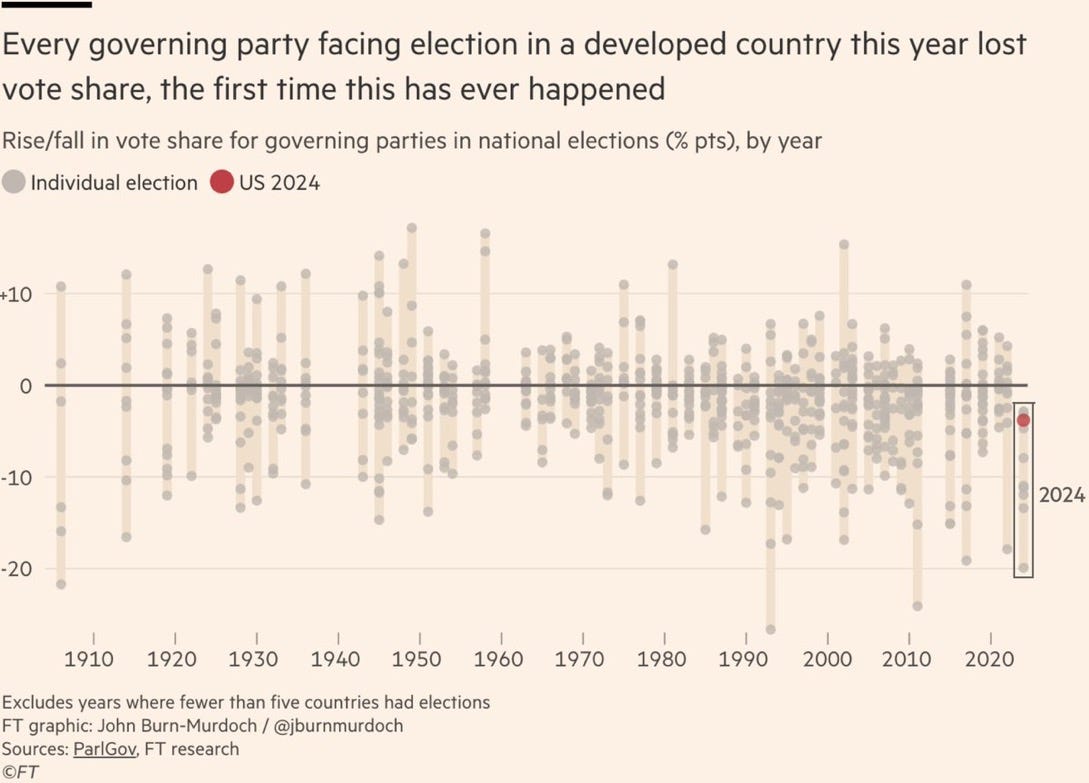

But those last two are more US-specific considerations, which glosses over the fact that the US election result was far from unique. The Financial Times found that, for the first time, every country that’s had an election this year has seen the incumbents lose support - most have been kicked out, while a few have been returned with a smaller margin. (And if you go back to last year, New Zealand was also part of that trend.) In fact, in this context the swing in the US vote was a relatively small one, perhaps reflecting the fact that they’ve come closer than anyone else to achieving the fabled ‘soft landing’ for the economy.

The pervasiveness of the swing in voter sentiment makes it obvious that it hasn’t been a left/right thing either; it’s really more of a backlash against incumbents - people have had a tough time in the last couple of years and they want to punish someone for it. And the one experience that has been near-universal was a bout of high inflation.

This might seem a bit of a rough deal for the ruling parties, given that (1) the responsibility for managing inflation has been very intentionally been taken out of the hands of politicians and placed with independent central banks, and (2) those central banks have in fact managed inflation down again. For instance, in the US the personal consumption deflator (the Fed’s preferred inflation measure) peaked at 7.2% in 2022, but has come down sharply since, and has been below 3% since late 2023. It’s not quite back to the 2% that the Fed aspires to, but it’s close enough - the inflation surge is effectively yesterday’s story. But the public perception is that we’re still in a ‘cost of living crisis’.

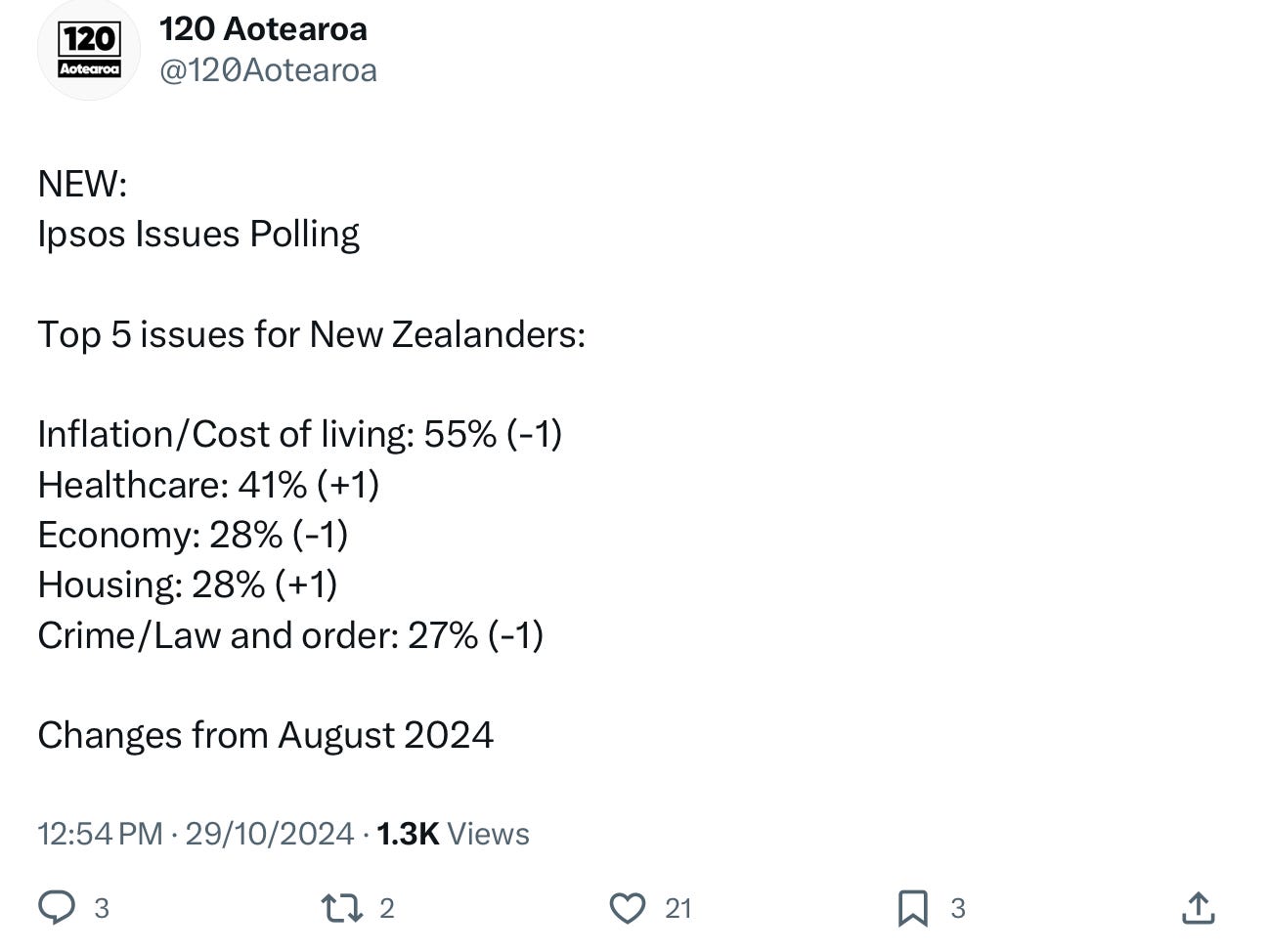

We see it here as well: this recent Ipsos poll found that the number one concern for New Zealanders, by a wide margin, is still inflation/the cost of living. And it has barely moved despite the fact that this survey was held after it was reported that the inflation rate had dropped back sharply to 2.2%.

So why is inflation still seen as an issue? I think there are at least two major ways in which the general public may not feel about inflation in the same way that economists do.

1: Price levels vs rates of change

In the standard framework for monetary policy, what matters most is the expected rate of inflation. If people believe that overall prices will rise by 2% next year, they will act accordingly today, which in turn ensures that the actual result is likely to be close to that mark. If the general level of prices actually rose by 10% last year, that rise is treated as ‘bygones’, other than the extent to which it affects expectations about next year’s inflation rate.

But there is evidence, at least anecdotally and in some surveys, that the level of prices does play a role in people’s thinking. That also shows in the way that the terms ‘inflation’ and ‘cost of living crisis’ are often used interchangeably - when people talk about high inflation they’re often really saying “my cost of living went up a lot and it hasn’t come down again”.

There isn’t really a hard and fast answer about how price levels vs changes play into people’s thinking. For instance, I don’t imagine that voters still hold a grudge about the fact that food prices1 rose by quite a lot in the 2000s and never came down again. But I do remember that through the 2010s there was an ongoing refrain that “food just keeps getting more expensive”, even though food prices were actually pretty flat through that period. Indeed, you could even argue that food got cheaper through the 2010s, since it rose by less than the general rate of inflation. And it certainly got cheaper relative to rising incomes. But that brings us to the second point of difference.

2: Nominal vs ‘real’

Most of the US economists that I follow on Twitter are Democrat-leaning, and before the election they would frequently argue that wage growth has actually outstripped inflation over Biden’s term. While that wasn’t true in the initial period after Covid, ‘real’ wages have since turned higher and have more than made up that lost ground. (And given their leanings, this point has often come with an undertone of “what are people complaining about, the economy’s doing great”.)

But this message of “you’re actually ahead of the game!” clearly hasn’t resonated with voters. For one thing, it may not even be true - Zac Mazlish has a post showing that if you use more appropriate measures of wages and prices, the median worker may have gone backwards in real terms under Biden after all. And outside of the US, it’s clearer that real wages have fallen since Covid - wages are generally outpacing inflation today, but they haven’t made back the ground that was lost earlier.

There’s also some survey evidence that people don’t view things neatly in ‘real’ terms. For instance, workers tend to feel that a cost-of-living pay adjustment is something that they’ve had to work hard to earn, rather than something they’re entitled to. In a high-inflation, high-wage-growth world, that can leave them feeling like they’re on a hamster’s wheel, running just to stand still.

To be clear, I’m not saying that economists are looking at inflation the wrong way. Real wages define the budget constraint that consumers face, and expected rates of inflation affect the incentives that they face, so these factors still do a better job of explaining how people act - just not necessarily how they ‘feel’. In other words, they’re the right things to focus on when making economic forecasts, but perhaps not when making political predictions.

One last thought: if voters really do hold a grudge about past increases in the price level, it’s not just bad news for incumbents, it’s also an ominous sign for the parties that replace them. Once the general level of prices goes up, it’s very difficult to bring it down again - partly because central banks are tasked with preventing that from happening,2 and partly because wages are very inflexible downwards and they make up a large part of the cost of goods and services. As a result, your options for getting a meaningful fall in prices would seem to be limited to:

A severe recession, more than the central bank has the power to offset - which isn’t going to be popular with voters either;

Getting lucky with, say, a sharp fall in world oil prices; or

A rise in labour productivity, which would reduce costs while boosting wages. No doubt every political party would wish for this, but none of them have found the formula for it.

Things like food and fuel prices are seen as highly ‘salient’ to people’s perceptions of inflation. Because we buy them frequently, we’re more aware of it when prices are rising or falling quickly.

That doesn’t have to be the case; central bank targets could instead be specified in terms of maintaining a price level, so that any overshoot has to be reversed in the future. While the idea of a price level target does have its fans, I think in most circumstances it would create more problems than it solves.