The RBNZ takes on the house

The RBNZ worries that a re-emerging housing shortage could keep inflation stubbornly high.

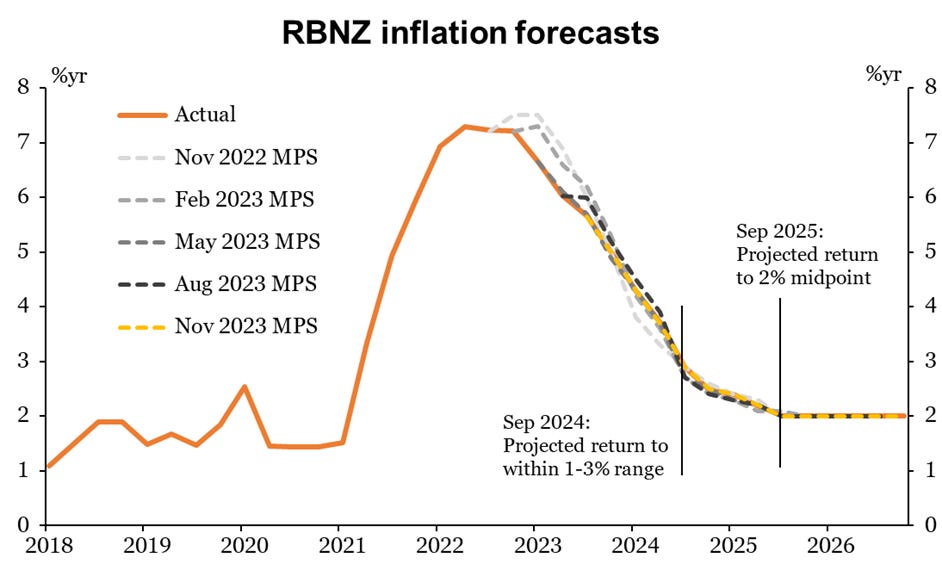

Yesterday’s Monetary Policy Statement was the last review for the Reserve Bank this year, and their last one for the next three months. Just like in August, they will have surprised many people with the strength of their concerns about inflation, and with their projections that if anything the Official Cash Rate might need to be higher again next year.

By way of explanation, the otherwise very brief news release notes that:

While population growth has eased supply constraints, the effects on aggregate demand are becoming apparent. This is increasing the risk of inflation remaining above target.

I’m only casually following the data these days, so at least to me it had not reached the level of “apparent”. Curiously, it was only in August that the RBNZ was mounting a case that population growth would be less inflationary than usual this time, due to the composition of the migrants. I wasn’t convinced, but I also don’t think that three months is enough evidence to prove it wrong.

On reading further, it seems that the RBNZ’s specific concern is around the re-emergence of the housing shortage. Net inward migration has surged to all-time highs, just as the pace of homebuilding has started to fade.

Housing market pressures can directly enter the Consumer Price Index in two ways. The first is rents, which have indeed picked up some steam in recent months, as the chart below shows.

Rents make up a large share of the CPI - just under 10% currently. But the way that they’re measured in the CPI means that they evolve fairly gradually over time, which means they don’t account for much of the variation in inflation. If rental inflation were to rise from say 3% to 5% - historically quite a rapid pace - it would still only add 0.2 percentage points to the overall inflation rate. That’s not enough on its own to account for meeting or missing an inflation target that’s 2 percentage points wide.

The second direct channel is prices for new home builds. This is also a very large item - another 10% of the CPI - and unlike rents, it does vary quite a lot over time. Homebuilding inflation peaked at 18.3% in the year to March 2022, in the wake of the post-Covid housing boom and the worst of the shortages in building materials. Prices are still rising, but the pace is slowing - down to 5% in the past year, and just 0.6% in the last quarter.

As the chart below shows, new build costs have a pretty close relationship with sale prices for existing homes. That need not necessarily be the case. For starters, they’re not actually measuring the same thing: the CPI item is specifically about the price for a new house, whereas sale prices capture the value of both the house and the section. Indeed, a lot of the action in ‘house’ prices is actually driven by the land - specifically the redevelopment potential of that land - rather than the value of the building that’s currently on it.

But I think there’s good reason to believe that the relationship is both real and causal. New homes and existing homes are close substitutes. When the demand for housing increases, buyers will first bid up for the properties that are already available. That in turn gives builders the leeway to increase their prices, once the aspiring homeowners start knocking on their door. That doesn’t necessarily mean that builders will be milking it, though: what tends to happen is that businesses across the length of the supply chain lift their prices too, depending on the extent of competition in their segment of the market.

What would happen if build costs rose on their own, without a preceding rise in sale prices? New homes would quickly be priced out of the market; the rate of homebuilding would slow; the housing supply would eventually fall behind demand; and existing home prices would be bid up anyway.

So to my mind, if you’re worried about a resurgence in building costs, you must also worry about a resurgence in house prices. The RBNZ is now forecasting house prices to rise by about 5% a year in the coming years… which would actually be a pretty well-behaved outcome (about in line with household income growth). But as I know from bitter experience, picking the magnitude of house price movements is much harder than picking the direction.

Rising house prices also have an indirect impact on the CPI, by boosting consumer demand via the ‘wealth effect’. I feel like this has been explained ad nauseum, so I’ll leave it there.

On a less important note, there was a comment in the record of the meeting that caught my eye:

Some members noted that inflation has now been above target for some time, and that there should be a low tolerance for any increase in the time to return inflation to target.

Yes, it looks like it’s going to be a long time outside the target range… but no more so than was expected at any point in the last year. In every statement since November 2022, the RBNZ’s forecasts have had inflation dropping below 3% in the September quarter of 2024, and reaching the 2% midpoint of the target range a year after that. And those forecasts were all predicated on pretty much the same path for monetary policy - it was in November 2022 that the RBNZ first signalled that the OCR would reach 5.5% this year.

So even though inflation is going pretty much to plan, it seems that some committee members are getting angsty about the plan. It’s one thing to anticipate an outcome, and another thing to live through it. In monetary policy we talk about ‘time inconsistency’, but it seems to be a problem in life in general: we’re just really bad at predicting how we’ll feel about things! (This was the gist of psychologist Daniel Gilbert’s Stumbling on Happiness.)

The ‘low tolerance’ comment is an echo of the Reserve Bank of Australia, which lifted its cash rate again in November after several months of steady-as-she-goes messaging. The difference, though, is that the RBA only ever aspired to do the bare minimum to meet its inflation target. Even now, its forecasts have inflation only dipping below 3% at the end of 2025, another two full years away.

As the RBA is (re)learning, the danger with only aiming for the very top or bottom of your target range is that it leaves you no room to absorb any bad news along the way. In contrast, the RBNZ have at least been plotting a path back to the middle of their target range, which would give them more wiggle room to deal with surprises in either direction. So far they’re on track… but there’s still a long way to go.

Anyway, I have another post coming tomorrow on the economics of innovation. I aim to alternate between timely data-focused pieces and longer thinky ones, but I haven’t been great at sorting a schedule.

The house always wins... in the end.

RBNZ's sharp rise of interest rates by 4%+ in the last 2 years to current levels is in no small part responsible for the re-emerging housing shortage and increased the cost for developers to supply new builds. So to use that as a reason to keep rates higher for longer seems self defeating. With current mortgage rates at around 2-3% p.a. higher than the pre-Covid era developers struggle to get the numbers to work plus there are a lack of buyers that qualify for the mortgage at current mortgage rates. Other potential and existing property investors lack the confidence to invest to provide more new build rental stock, especially in light of RBNZ's consistent 'higher for longer interest rates' storyline.

RBNZ's stance may even contribute to keep inflation stubbornly high as a result of the ongoing reduction in new builds from being built, therefore adding upward pressure to rents and of course ultimately house prices.

After all...

The house always wins in the end.