Is New Zealand the toughest on foreign investment?

Is New Zealand the toughest on foreign investment?

Tracing the origins of an often-repeated fact.

A couple of months ago the OECD released its latest Economic Survey for New Zealand, and its chief economist was in the country to promote its key findings. I went to one of the presentations, along with a small handful of business and government representatives, which made for a lively and varied discussion afterwards.

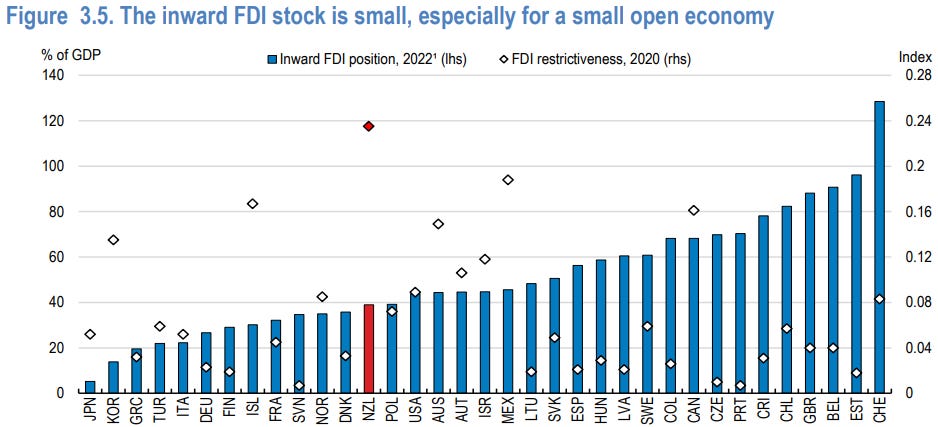

There was one particular finding from the OECD report that seemed to resonate with everyone else in the room: the idea that New Zealand has one of the most restrictive regimes in the world when it comes to foreign investment. In fact, on the measure that the OECD has constructed, we’re the most restrictive of all of its member countries. Here’s the chart from their report:

I’ve seen this measure cited before, and each time my reaction has been: Really? I mean, I can buy that we’re more restrictive than is necessary. But the most restrictive? Surely there are plenty of other contenders for that title. But my group was quite taken with the idea. Everyone has stories of foreigners with tens or hundreds of millions of dollars to spare that they would love to invest in New Zealand, if only we didn’t make it so hard for them.

What’s more, if you go to the OECD website, you can see how this measure has evolved over time - or not, in our case. Based on the current methodology (this will be an important point later), our score basically hasn’t changed over the last 20 years, even as the rest of the world has generally become more liberal. Heck, China is now more open to foreign investment than we are, if you believe this measure.

So I decided it’s time to go back to the source material, to try and understand how the OECD is coming to these judgements and whether there’s any obvious reason for scepticism. The answer turned out to be a bit more convoluted than I expected.

What is this thing anyway?

The measure I’m referring to is called the foreign direct investment (FDI) restrictiveness index. The OECD has been producing this since 2003, initially just for its member countries, but it has expanded its coverage and frequency over time.

First, a couple of things to help define the scope of this index. “Direct” investment refers to when an investor takes what would be considered a controlling stake in a business or an asset (the rule of thumb is a greater than 10% share of ownership). In these cases the investor is typically providing more than just money - they may also bring managerial expertise, access to technology, and global connections. There’s also more of a sense of a long-term commitment - typically they’re buying into unlisted assets, so they go into it aware that they won’t be able to cash out easily.

The other key word is “foreign”. There are many things a country can do to throw up barriers to investment. It can tax business income at a relatively high rate; it can bog things down in onerous resource consent processes; it can take a hard line on mergers and takeovers for anticompetitive reasons. But to the extent that these apply equally to local and foreign investors, they don’t contribute to a country’s score on the restrictiveness index.

The OECD assesses a country’s rules on foreign investment and tries to quantify their impact, producing a score between 0 (completely open) and 1 (effectively closed). The overall score is the sum of four categories:

Limits on foreign ownership. This is the easiest one to quantify: limiting the share of an asset or business that a foreign investor can own. If a country blocks overseas overseas holdings altogether, it’s given the maximum score of 1 for this category (and the other categories become redundant). The score is lower if a country blocks majority ownership, or otherwise caps it below 100%.

Screening and approval requirements. A country may require a foreign investor to seek approval first. That means they may be subjected to a range of tests: for instance, a potential investor may be required to show that there will be a net economic benefit to the country. It also means that the government may have the discretion to turn down an investment if it’s not deemed to be in the ‘national interest’. The maximum score for this category is 0.2.

Restrictions on foreign personnel. A country may block or limit a foreign investor’s ability to bring in its own managers and directors from overseas. The maximum for this category, a complete ban, is 0.1.

Operational restrictions. This can range from restrictions on land ownership, to reciprocity requirements, to limits on the ability to send profits back overseas. Most of these measures are scored pretty low on their own, but they’re cumulative; the total score for this category can be 0.4 or more.

Rather than calculating a single country score, the OECD calculates these scores at the industry level, then works out a weighted average. That’s because countries are often less open to foreign ownership in certain areas, such as land or natural resources, industries that are dominated by a few large players, or areas that are deemed to be critical infrastructure.

They also, to the extent possible, allow for the fact that a country may apply different rules geographically. For instance, within the European Union, there are few or no restrictions on investments between member countries, but they may restrict investors from the rest of the world. As a result, every member country is scored lower than the EU would be as a bloc.

As you can probably tell by now, there are a lot of judgments that have to be made in calculating this index - the most important one being how to quantify rules that are mostly qualitative in nature. (And the scoring is only based on the rules themselves; the OECD doesn’t even attempt to record how every country applies its own rules in practice.)

I certainly don’t envy the OECD in this task. On the other hand, it’s a burden that they’ve chosen to place on themselves - it’s not as though there was a gap in the market that needed to be filled by this index. So I don’t feel we need to give them a pass on this stuff just because it’s hard.

Why are we scored so highly?

This is where things get a bit fiddly. The OECD’s restrictiveness index originates from a 2003 paper. This work was more limited in scope than the current index, covering only the OECD countries and just nine industries, mostly in services.

What’s notable is that in this original version of the index, New Zealand wasn’t considered to have anywhere near the most restrictive regime. Our overall score was 0.189, only slightly above the OECD country average of 0.175. Australia was well above us at 0.270; the scores ranged from 0.064 for the UK to 0.390 for Iceland.

Interestingly, this paper also provided some estimates going back to 1980. Despite the reputation of “Fortress NZ” at the time, we were scored as only slightly more restrictive than average back then as well (0.394, versus an average of 0.377). The deregulation between 1980 and 2000 was about in line with the rest of the pack.

Where we were scored highly - and this has always been the case - was in the second category, screening and pre-approval requirements. In contrast, for most countries the largest part of their restrictiveness score comes from the first category, limits on foreign ownership. New Zealand is one of the least reliant on this relatively blunt tool.

In 2006 the index was updated to include more countries and industries, but the scoring method was left largely unchanged. Again, New Zealand’s score of 0.170 was only a little higher than the OECD average of 0.148. One thing to note is that the legislation that currently governs New Zealand’s foreign investment regime, the 2005 Overseas Investment Act, was in place by this time. The OECD obviously didn’t consider this to be more restrictive than what had come before it.

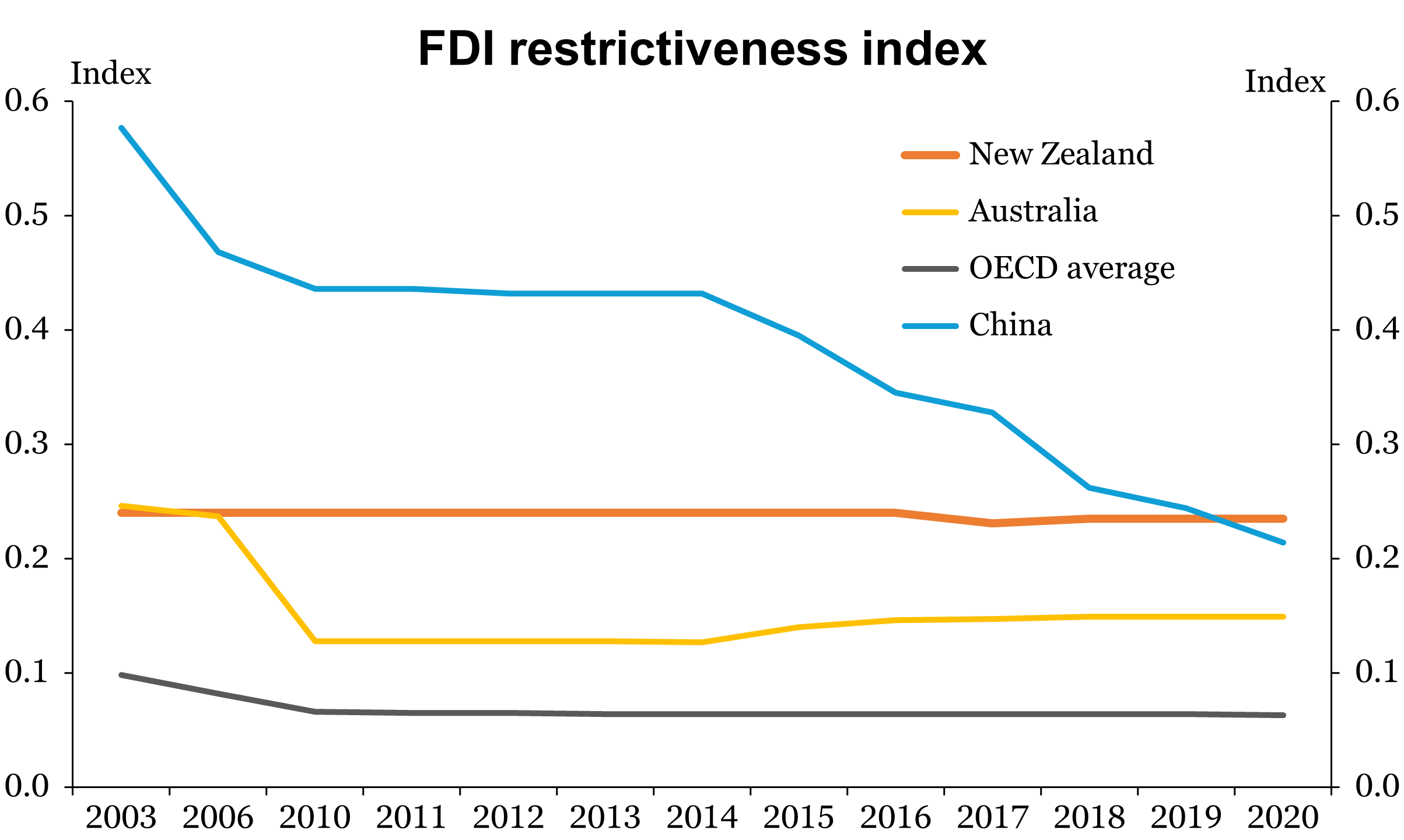

Things change, though, when we get to the 2010 update, which made a number of changes to the scoring system. Most significantly for New Zealand, it introduced a two-tier ranking for pre-approval requirements. If a country requires pre-approval for investments in assets worth less than US$100m, it’s given the maximum score of 0.2. If the threshold for pre-approval is above US$100m, the score drops down to 0.1.

Whether by coincidence or not, that’s right in the range that affects us. New Zealand requires pre-approval to acquire more than 25% ownership in an asset worth over NZ$100m - that’s about $60-80m in US dollars, depending on where the exchange rate has been over the years. And it appears that, simply by having this threshold at all, we were given the maximum score of 0.2 across the board, regardless of how many investments were actually captured by it. That pushed our total score up to 0.263, which is more or less where it has remained since.

Given that the whole point of the restrictiveness index is to provide international comparability, there’s an obvious flaw here. The same US$100m threshold is applied to every country regardless of their size, from the world’s largest economy of the United States, all the way down to Iceland (the only other country was given the maximum score for pre-approval restrictions).

The OECD’s justification for this is that “it could be argued that the average firm size is independent of the overall size of the economy”. But this doesn’t have to be “argued” at all; it could be measured and tested, and would almost certainly be found wanting. It’s true that exporting businesses can outgrow their home market, but most businesses are not exporters.

So I’m not a fan of the OECD’s index as it currently stands; the two-tier system means that it penalizes small countries for being small. The original scoring method seems closer to the mark; I would guess that New Zealand today would be above-average but not at the top of the range, and probably comparable with Australia.

Could we do better anyway?

To be fair, our $100m threshold for pre-approval is also quite arbitrary, even if it is at least in proportion with the size of the country. What’s more, it hasn’t kept pace with the times. Our annual GDP is two and a half times larger now than it was in 2005, thanks to a combination of real economic growth and inflation. The value of any asset that an investor might be interested in has probably risen by a lot more than that, due to a trend decline in interest rates over that time.

So at the least, there’s a case for reviewing the threshold - but perhaps we should instead use the opportunity to consider whether we need a screening regime at all. As I mentioned earlier, most OECD countries don’t go down this route, so there isn’t much international evidence on how restrictive it is. You could argue that it’s not a big deal in New Zealand by pointing to the fact that very few OIO applications are actually declined. But the issue we’re grappling with here is about the dog that didn’t bark - how many potential investors were put off even trying by the thought of months of hearings, thousands of pages of paperwork, and the risk of becoming the target of lobby groups?

Where other countries seemed to have landed is that investor screening is not so much restrictive as it is redundant. If the main concern is bad behaviour, we always have the power to regulate what a foreign-owned business gets up to within our own borders. Now there are limits to how far this argument applies - which is probably why it’s common for countries to restrict foreign involvement in the fishing industry, for instance. But on the whole, it’s a more practical solution than trying to identify the ‘good’ ones and hoping that they’ll continue to play nice once you’ve let them in.

Let’s say that we ditched our investor screening regime (and didn’t replace it with some other restrictions). That would bring our restrictiveness score down towards the OECD average of about 0.06. What sort of outcomes should we expect from that?

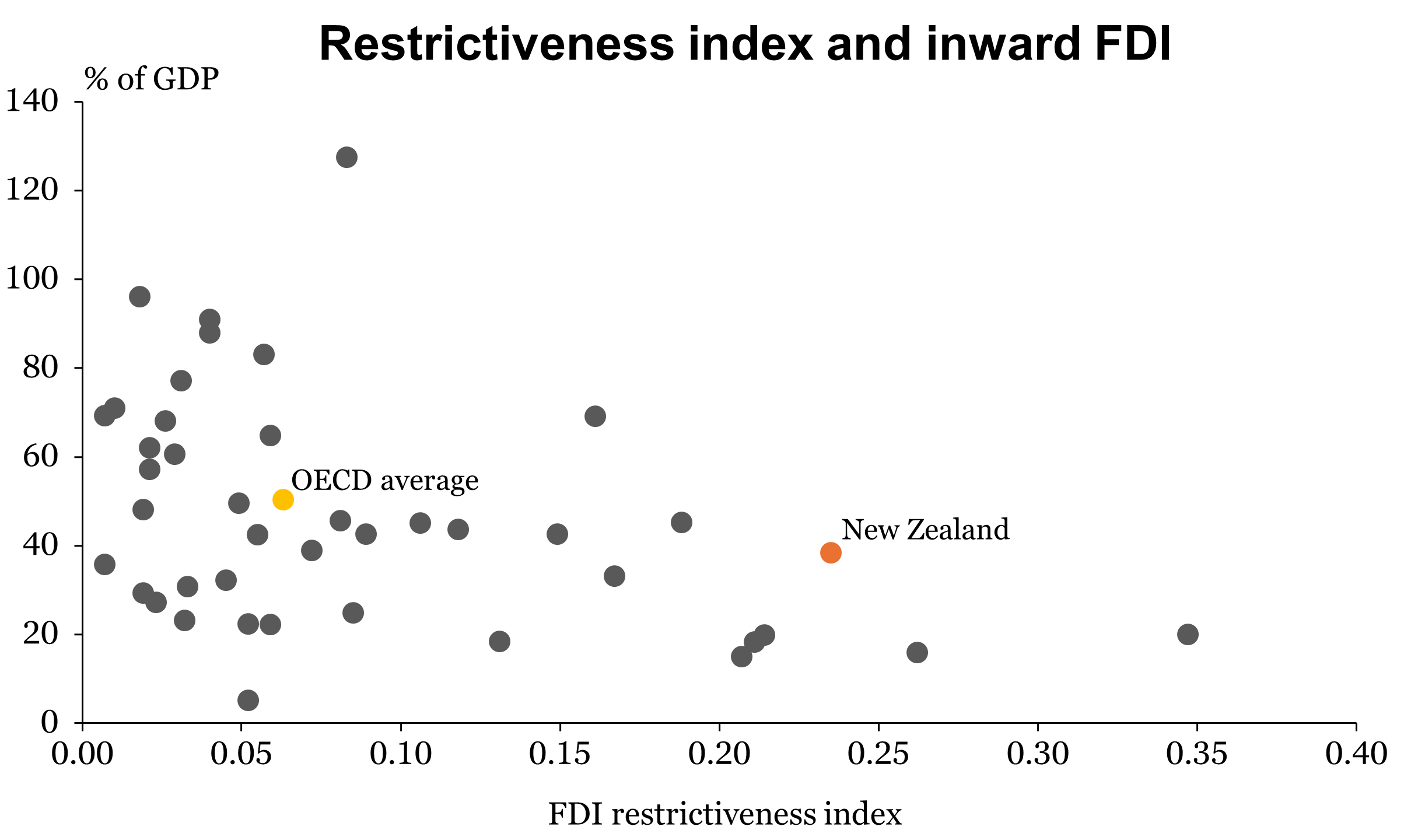

Think back to that chart at the beginning. I’ll show it again here in a different way, with the two series on different axes. (I’ve also included a broader set of non-OECD countries.)

There’s a clearer relationship on the right-hand side of the chart: countries with higher restrictiveness scores tend to have lower levels of foreign investment. But for countries with low restrictiveness scores, there’s a wide range of possible outcomes. The OECD average for the stock of foreign investment (50% of GDP) isn’t a great deal higher than our own (38%). And the country with the highest level (Switzerland) is deemed to be more restrictive than the country with the lowest (Japan).

Clearly there’s much more that goes into determining a country’s level of foreign investment. And the OECD’s own research shows that to be the case. This paper from 2019 finds a statistically significant relationship between the restrictiveness index and a country’s level of inward foreign investment, but the effect is not very large. The size of a country’s economy (or more accurately its scope), and the geographic distance from its major markets, have a far greater influence.

There is one final sense check we can do. If the rest of the world is more welcoming of foreign investment than we are, then we might expect to see New Zealand fare better on outward investment compared to inward. In fact it’s just the opposite: we’re right at the bottom of the range on outward investment, at a pitiful 8% of GDP. That strongly suggests that there’s something else behind our low levels of cross-border investment, something that applies in both directions - with size and distance again being the obvious candidates.

Does it even matter?

Throughout this piece I’ve glossed over the question of whether more foreign investment is even a desirable thing. Most studies have found that it has positive effects for the economy - for instance see this NZIER report from 2016 which gives a brief overview of the literature - and I don’t have a bone to pick with that work. Perhaps a more nuanced read is that foreign investment is more likely to be beneficial if you’re also getting the basics right - strong legal frameworks, low levels of corruption, etc. New Zealand generally scores quite well in these areas.

In conclusion

I’ll be honest, I went into this hoping that it might be an opportunity for a good old debunking. But as I read further, I went back and forth on whether that was really the right angle. I think the OECD’s ranking itself is flawed, but it touches on a valuable point. Given the insurmountable hurdles of size and distance, we can’t afford to settle for being “in the pack” for the things that are within our control - things like the quality of our regulations. A little less benchmarking, and a little more willingness to experiment, is needed if we want to improve our long-term economic performance.